Retirement Planning

Three Rules to Help You Avoid Poverty in Old Age

It’s only human to want to spend now, so best to make an iron-clad plan

Building financial security is a constant exercise in overcoming our dislike of delayed gratification.

Saving a portion of our salary today for a retirement that is decades away is a big ask, when we have all sorts of ideas of how to spend those dollars today.

In wonky academic circles, this very human habit is called present bias: When faced with a decision, we give more weight to what will feel best to us right now, rather than make a choice that will be smarter for us over the long term.

Like other behavioral biases that can mess up your life, the solution isn’t to unlearn or overcome this habit. We are who we are. Rather, consider steps that will help you work around the bias.

Make your savings automatic. If you have access to a retirement plan at work, having your contributions automatically deducted from your paycheck and sent to your 401(k) or 403(b) account puts saving for your future on auto-pilot.

You can do the same with an individual retirement account (IRA). Every discount brokerage will be happy to help you set up an IRA that automatically pulls money from your bank account every month or quarter.

Same goes for any savings goal – emergency fund, down payment fund. Set up a separate savings account and arrange for automatic deposits to be zapped from your checking account.

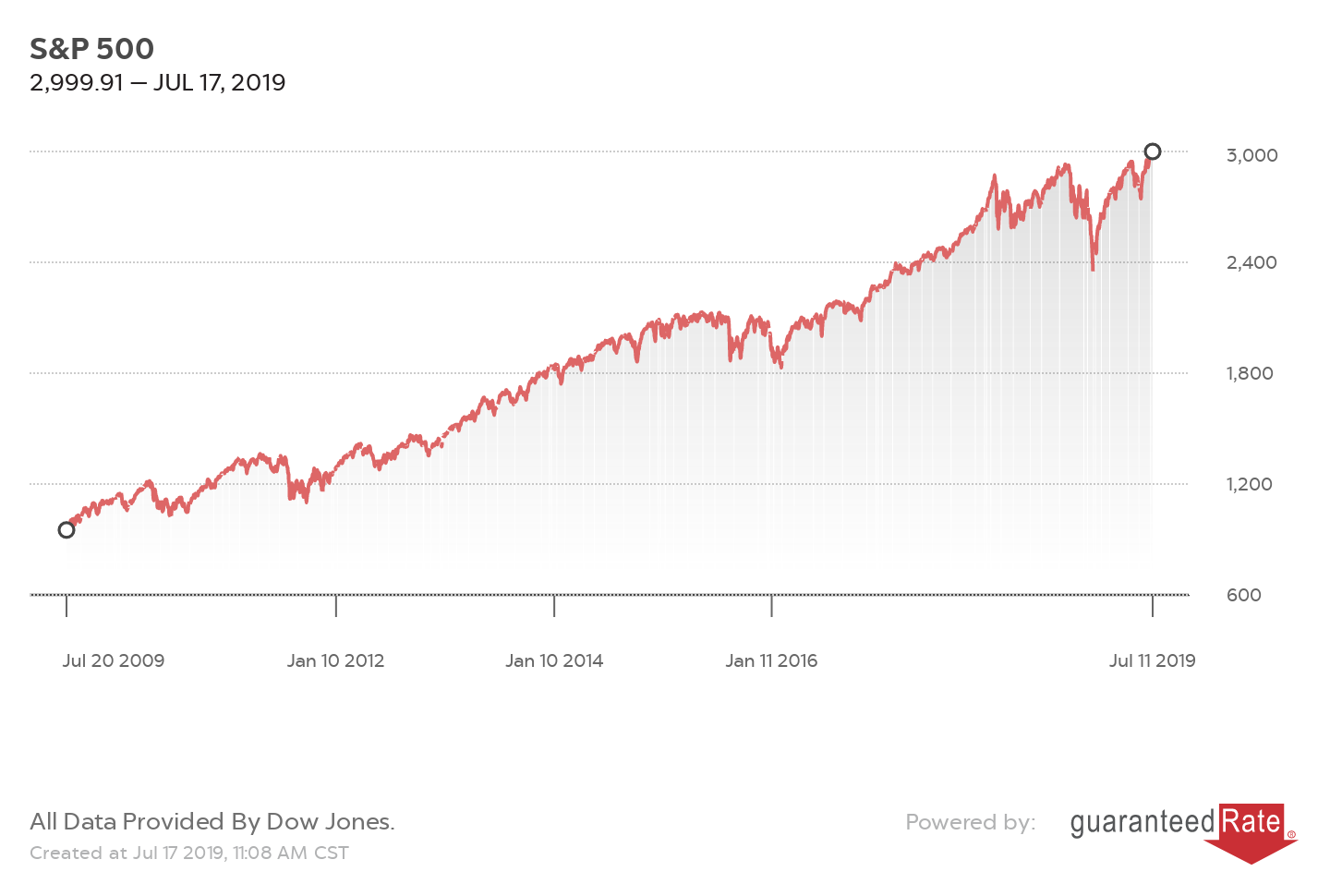

Write a mini investing manifesto. Our focus on the present can wreak havoc when a bear market hits. Watching your stock portfolio fall 20%, 30% or more is stressful, and it can lead to a desire to sell stocks. That’s market timing, and it’s exactly the opposite of what will serve you best in the long-term. For many investors, getting out at the bottom of the last stock market plunge meant they missed the incredible rebound in stocks that typically follows a plunge.

Research has shown that creating a “Ulysses Contract” can help us stay committed to a long-term plan. No need to tie yourself to the mast to avoid the Sirens’ call. Rather, create a one-page document of why you are invested. What’s your goal? Why have you chosen to invest a portion of your portfolio in stocks? Sign and date the document; a little formalization can be a helpful cue. Whenever you are contemplating making an investing decision – such as heeding your flight bias during bear markets – pull out your contract. Reminding yourself about your long-term goals can be the pause button you need to avoid giving into your present bias.

Envision your older self. Academic research has shown that we tend to treat our future self as a stranger whom we keep at arm’s length. Establishing a bit of a connection with our future self can be a great motivation to think about steps we can take today that will help us be kind to our older self. In one study, college students shown a doctored photo that aged them many decades opted to save a lot more for retirement. In another study, people who were primed to think about their self 20 years from now committed to working out more today.

If you could use a bit of a nudge to connect to your future self, give the AgingBooth app a spin. And consider giving pride-of-place to displaying family photos of older relatives around your home. Subtle cues to think about aging can help you make choices today that will pay off in the future.