Personal Finance

Smart Financial Moves for Your 30s and 40s

One of the greatest luxuries at any age is worrying less – here’s how to achieve that

As you enter prime earning years, financial decisions have bigger consequences. It’s nice to leave the ramen-eating, apartment-sharing phase of life. But with that growing salary, you’ll be buying a house, raising kids, continuing to pay off student loans – all while saving for retirement. Lots to think about.

Seven tips for building security in your 30s and 40s

1. Save at least half of every raise. This is the time in your career when you’ll get promotions or move on to bigger and better jobs. One of the best favors you can do your later-life self is to make a formal commitment that you’ll save at least half of every raise. Write it down. If you get a 5% bump, earmark at least 2.5% for savings. Ideally more. Boost retirement savings, build emergency savings, or pay down student loan, car loan and credit card debt.

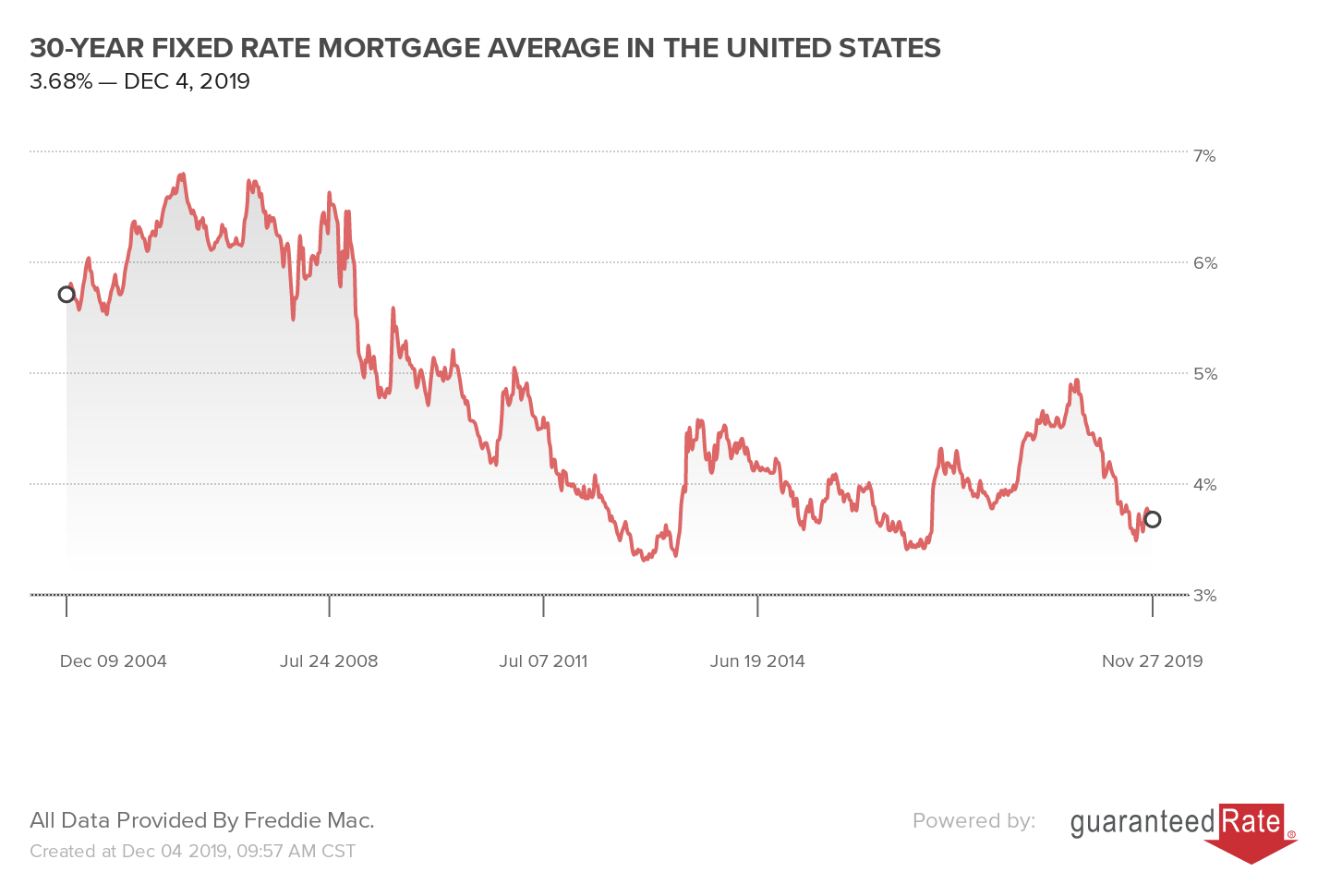

30-Year Fixed Rate Mortgage Average in the United States provided by Rate.com

2. Don’t wait any longer on retirement. Hopefully, you got serious about saving for retirement in your 20s, giving you the longest time to take advantage of compound growth. If not, you want to get to a 15% savings rate ASAP. Wonks have run the numbers: If you don’t start saving until your 30s, you will need to plow at least 15% of your income into retirement accounts if you want to hit your 60s in solid financial shape.

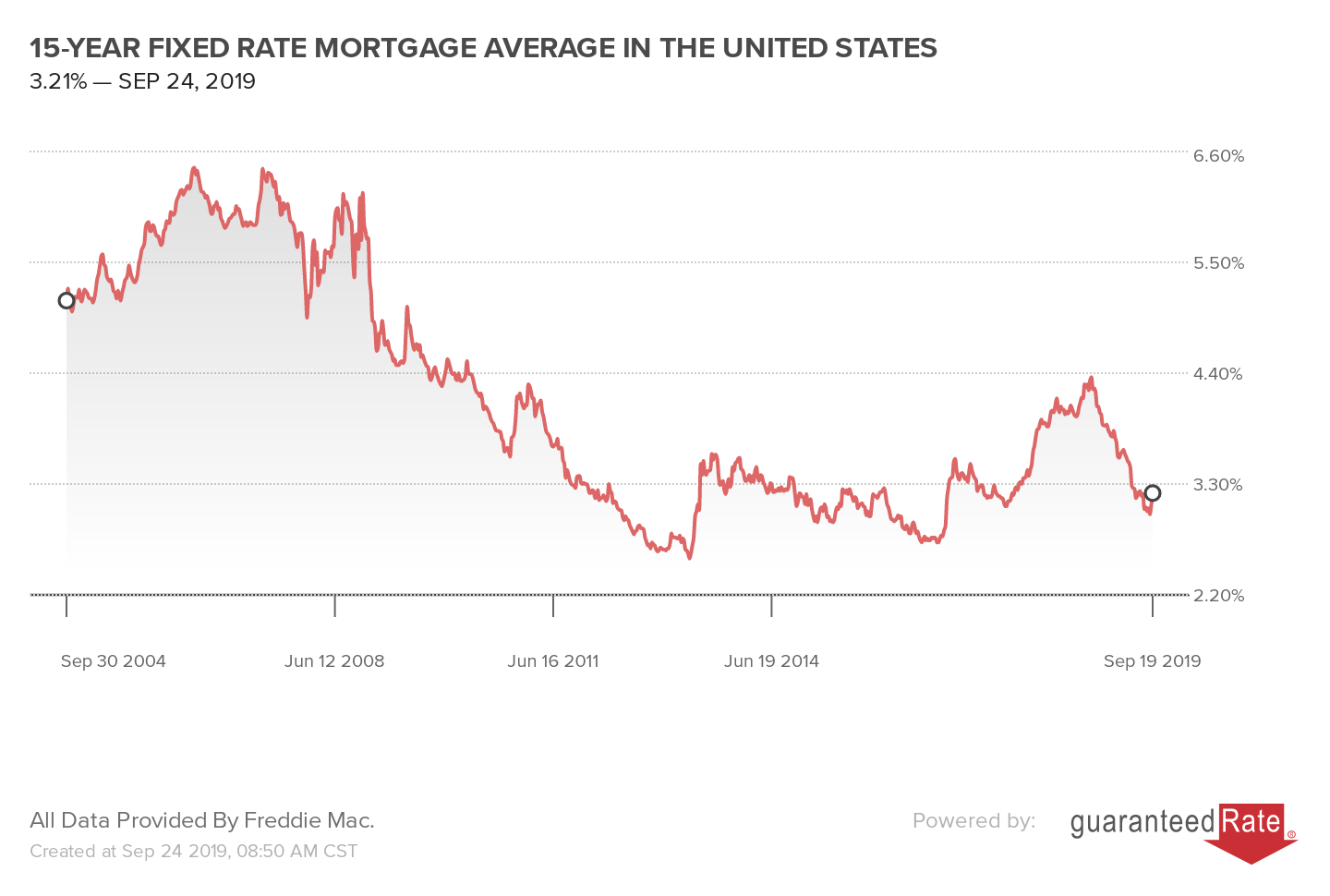

15-Year Fixed Rate Mortgage Average in the United States provided by Rate.com

3. Consider a 15-year mortgage. The advantages: a fixed interest rate about 0.70 percentage points less than a 30-year; tens of thousands of dollars less in interest over the life of the loan. Be done with one of your biggest expenses before you hit your 50s. That gives you cash-flow flexibility to scale back work or pay for the kids’ college.

Yes, the monthly payment on a 15-year is higher. And it makes no sense to take on a payment so large you can’t save for retirement. But if you’re just now forming a home-buying strategy, you can consider buying a less expensive house.

4. Beware lifestyle creep. In your 20s, you still needed to eat, commute, look presentable at work, and take a burn out-avoidance vacation from time to time. You did it all on a tighter budget than you have today.

No one is suggesting you go all miserly, but recognize that every choice to spend more today is a decision to save less. Like your car: the average monthly new-car payment is more than $500. If you instead kept your car loan budget to $300 or so – buy a used car, be less stylish – you’ve just freed up $200 monthly for other uses.

5. Hands off the 401(k) when you job hop. When you leave a job, you’re allowed to cash out your 401(k). Huge mistake. A dollar spent today is a dollar-plus you won’t have for retirement. You will have to save much more to make up for what you didn’t leave to compound. You’ll also owe a 10% penalty on the withdrawal, and if you’re in a traditional 401(k) you’ll owe taxes.

Money you’ve saved for retirement should be kept growing for retirement. If your account has at least $5,000, you can leave it with your old employer. Or your new employer may allow you to roll over your savings into your new plan. Or open an IRA account at a discount brokerage -- called a 401(k) or IRA rollover. There is no tax due.

6. Move college saving down your to-do list. Once you have kids, a logical goal is to start saving for their college years. But logical may not be smart. If you still have student loans or credit card debt, or don’t yet have a sizable emergency fund, or haven’t gotten serious about retirement, you have no business saving for your college.

Building a sound financial base will allow you to weather layoffs, illness and all the “what-ifs” that can emerge. As for college, there are affordable federal student loans for your kids (not to be confused with pricey private loans from banks), and in-state schools that can be paid for with those federal loans.

7. Protect yourself and your family. Anyone dependent on your income? Spouse? Kids? Siblings? You need life insurance. Period. No excuses. And c’mon, buying term life insurance has never been easier or cheaper.